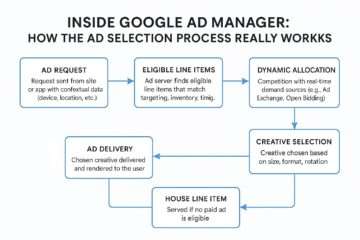

Google Ad Manager Ad Selection: How Ads Are Chosen and Delivered

Deep Dive: How The Trade Desk Leverages HUMAN Security for In-Platform Ad Fraud Detection

Comparative Analysis: DV360 vs. The Trade Desk (DSP Features)

Automation and AI in AdTech and Programmatic Advertising: Challenges and Opportunities

DV 360 Targeting and audience strategies important questions with answers

The Global Competition Between Connected TV (CTV) Demand via Display & Video 360 (DV360) and The Trade Desk (TTD): A Deep Dive into Platforms, Pros, Cons, and the Future of CTV Advertising

Top 200 Questions Related to Campaign Manager 360 (CM360)

DV 360 campaign creation and management question and answers focusing on building, launching, and managing campaigns.

Supply Path Optimization in Programmatic Advertising: Strategies and Real-World Examples from Ad Tech Leaders in India

Digital Out-of-Home (DOOH) vs. Connected TV (CTV): A Comprehensive Comparison and Future Programmatic Expansion

Google Sunsets “Video Games (Casual & Online)” Category in Ad Manager: Impact and Future Trajectory in Gaming Ads

Top 200 Questions on Google Ad Manager in Programmatic Advertising

Understanding the Major Differences Between CTV and OTT: A Comprehensive Guide

Top 200 Questions Related to CTV Programmatic Advertising

A Comprehensive Guide to Display & Video 360 (DV360): Features, Setup, and Integration

Amazon Prime Video’s Shift to Ads: Impact on CTV Advertising, Consumer Perspectives, and Ethical Considerations

Microsoft’s Acquisition of Xandr DSP and Transition to AI-Powered Advertising

Top 200 Programmatic Advertising Questions for DV 360 for Interviews

10 Mind-Blowing Programmatic Advertising Campaigns That Redefined Digital Success

The Rise of Gen AI Ads in Programmatic Advertising

Agencies and Supply-Side Platforms: A Strategic Alliance Reshaping Programmatic Advertising

Campaign Setup and Execution in Display & Video 360 (DV360).

Programmatic Guaranteed Deal Set Up under Google Ad Manager

Latest Updates and Enhancements in DV360 (March 2025)

Connecting GAM , GA4 and DV 360 for an a holistic growth of Publishers Property and database.

DV 360 Campaign Setup and Important questions based on campaign set up in DV 360 and Optimization.

Important Interview Questions for DV 360 (Part-4)

Important Interview Questions for DV 360 (Part-3)

Top 20 Question for Interviews in in Display and Video 360 (DV 360) for Interviews (Part-2)

Top 20 Question with answers for Display and Video 360 (DV 360) for Programmatic Advertising Interviews

Prominent Advertising Trends to Monitor

How to generate State Wise Reports in Google Ad Manager

Google loses an important antitrust fight over its search monopoly

Netflix is set to introduce its own advertising technology.

What Is Preferred Deal?

The Main Updates To Google Search Are Crushing Sites And Changing The Web

How Google Uses Cookies?

Google Ad Manager-Important Terminologies to know and Use.(Part-3)

Macro, Cache Busters and Click Macro what is it?

Google Ad Manager-Important Terminologies to know and Use.(Part-2)

Google Ad Manager-Important Terminologies to know and Use.(Part-1)

No Matter The Temporal Framework, Third-Party Cookies Will Cease To Exist.

The cookie less world will not become a reality in 2024 as per reports from Google.

The growth of digital advertising revenue decelerates once more in 2023, according to the IAB Ad Revenue Report.

According to the IAB, social video will surpass CTV this year.

Although Google’s Ad Network Business Suffers, Google Search business brings the bacon home.

Why Privacy Sandbox Examiners Feel Comforted Google postponed the death of the cookie

Key Justifications for Video Advertising’s Role in the Future of Marketing & Available Ad Types

Using Programmatic Video Ads: A Guide

DV 360 Reporting Dimension (Part-2)

Dimension Reporting in DV 360 (Part-1)

DV 360 Reporting Parameters- Metrics in Reports (Part-3)

How to Troubleshoot Floodlight Tags and Use Implementation Alarms

Essential Guidelines for DV360 Ad Campaigns

Floodlight Tag: What Is It? A Guide To The Media Campaign Analysis Tool Step By Step

DV 360 Reporting Parameters- Metrics in Reports (Part-2)

DV 360 Reporting Parameters -Metrics in Reports (Part-1)

Understanding first-party data and its marketing benefits

The Top Programmatic Advertising Platforms of 2024 for Publishers

Understanding the Implications of the Third-Party Cookie Phaseout

2024 Adtech Predictions: Overcoming Google’s Cookie Challenge, the Ascendancy of SSPs, and the Transformation of Retail Media

DV 360 Campaign Creation and Set Up – Step by Step Tutorial

DV 360 Insights- Features, Advantages and Limitations.

DV 360 Demo Video of Features and Functionalities

How to fetch reports in Google Ad Manager( GAM)

How to Create Tags for Mobile App via Google Ad Manager(GAM) for Publishers.

Programmatic Guaranteed Deals, Preferred Deal and PMP Deals under Google Ad Manager

Multiple Customer Management (MCM): What Is It?

Key programmatic advertising trends in 2024 which will act as a guide for future ads.

5 Optimal Strategies for Enhancing Marketing Efficiency in Programmatic Advertising

Programmatic Advertising PodCast with Madan Yadav from inMobi

DV 360 Important Questions Part-4 in Programmatic Advertising

Display and Video 360(DV 360) important questions (Part-3)

DV 360 Important Questions in Programmatic Advertising Part 2.

DV 360 Important Questions (Part-1)

Programmatic Advertising PodCast with Anant Chaturvedi

Digital Marketing and Artificial Intelligence. How AI can optimize the results better?

DV 360 Features

DV360 Adopts New Video Guidelines from the IAB Tech Lab. What Effect Would That Have On Buyers’ Wants for Video Ads?

How to Manage Call to Action Ads through Google Ad Manager.

VDO.AI Podcast

Google Ad Manager Dashboard Overview

Programmatic Advertising PodCast with Uwais Sheikh

Publisher Exchange Value Optimization in a Cookie-less Programmatic Ad World.

The growing importance of Adaptive Banner Ads in Programmatic Advertising.

The issue of Jobs in Programmatic Advertising and the reducing Pay Packages.

The Curious Case of Programmatic Advertising Revenue Fall in last 7 Months.

Programmatic Advertising Concepts

New Things to know about Header Bidding (Part-1)

Programmatic Advertising Question Series 3

Programmatic Advertising Question Series Part 4

Google Ad Manager Features

The Issues of Programmatic Advertising

Creation of Tags under Google Ad Manager

The Future of Programmatic Advertising in the AI ERA.

Google Ad Manager- How to Create New Ad Units and New Ad Unit Tags under Google Ad Manager

ALL ABOUT AMPHTML ADS IN Programmatic Advertising

Creatives under Order and Line Items in Google Ad Manager.

Programmatic Advertising Demo in Google Ad Manager- Orders and Line Items .

Google Ad Manager Dashboard Home Page Overview

The Importance of SiteMap in SEO and a Website.

The Future of Programmatic Advertising-Challenges and Opportunities

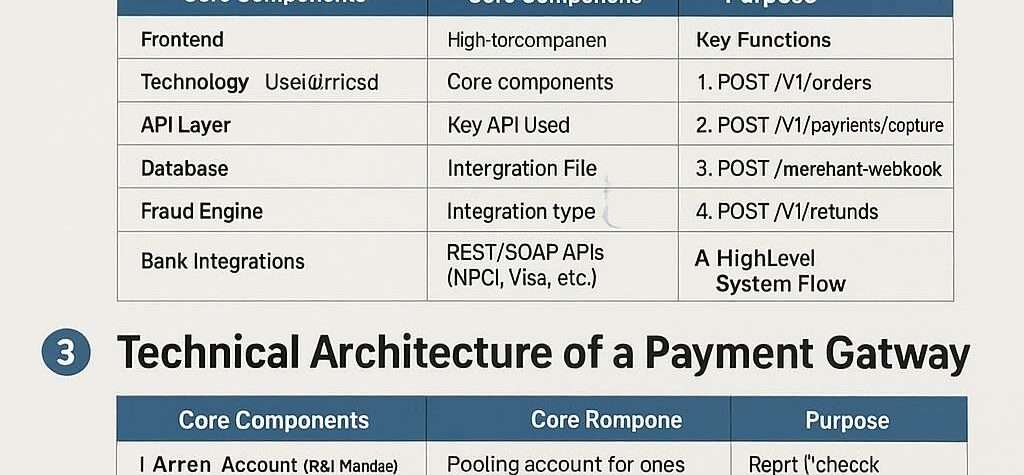

A Payment Aggregator (PA) acts as an intermediary between merchants, customers, banks, and payment networks, simplifying digital transactions. Examples include Razorpay, PayU, PhonePe, and Stripe.

Key Functions of a Payment Aggregator

Merchant Onboarding (KYC, underwriting).

Unified Checkout (supports cards, UPI, wallets, net banking).

Transaction Routing (connects to banks, card networks, and UPI).

RBI PA Guidelines (2021) – Mandates nodal accounts, KYC for merchants.

PCI-DSS – Ensures secure card data handling.

DPA 2023 (India) – Data localization requirements.

10. Case Study: Handling Failed Transactions

Scenario:

Customer pays via UPI, but money is debited without merchant confirmation.

Resolution Steps:

Check PA’s Transaction Status API (GET /v1/payments/{id}).

Verify Webhook Logs (if payment.failed event was missed).

Initiate Auto-Refund (if payment not captured in 7 days).

Conclusion

Payment Aggregators form the backbone of digital commerce, handling transactions, fraud checks, settlements, and compliance. Understanding their technical flows, APIs, and business models helps merchants optimize payments and reduce failures.