Although social video and connected TV advertising are expanding, their growth rates are not identical.

The initial segment of the annual report by the IAB concerning developments in digital video advertising strategy was published on Thursday. The report is based on a partnership with Guideline, which gathers media billing data, and an Advertiser Perceptions survey of digital video buyers and brands commissioned by the IAB.

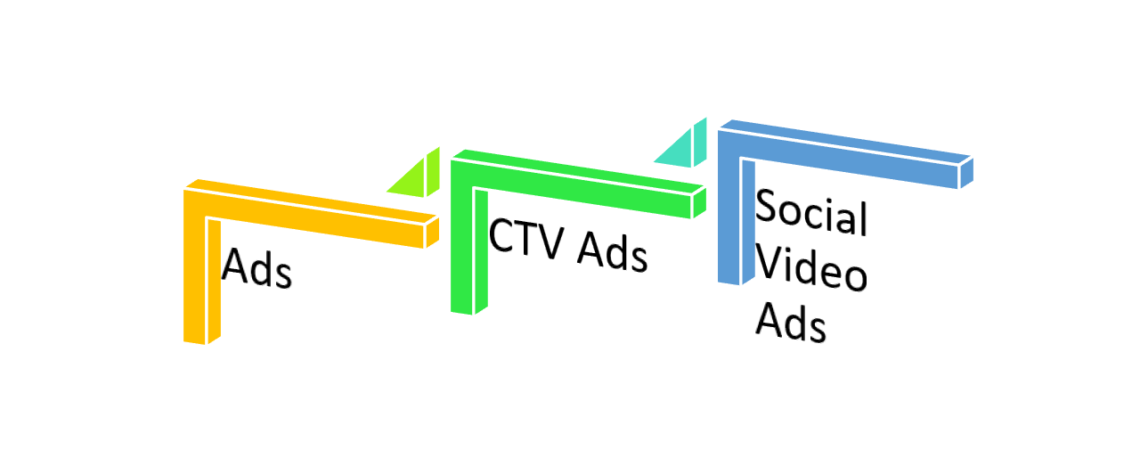

Digital video advertising expenditures, including social video, CTV, and online video, are expected to reach $63 billion in 2024, according to the IAB, a 16% increase from the previous year.

The report identifies three distinct categories of video advertisements, with social video emerging as the unequivocal victor.

Social video is anticipated to reach $23.4 billion by the end of 2024, representing a 20% annual increase. Conversely, CTV is anticipated to rise 12% year-over-year to $22.7 billion.

CTV lacks the ability to provide superior campaign reporting based on an advertiser’s preferable business outcomes, according to Chris Bruderle, vice president of industry insights and content strategy at the IAB. As a result, social video is “gaining ground on CTV.” Additionally, CTV lacks visibility into useful insights, such as which programs users are viewing or where an advertisement appears in a video stream.

Despite the fact that social media platforms face their own challenges with transparency (consider Meta and Google), at least they employ attribution. As a result of the strain on marketers to justify their investments by tying their ads to tangible outcomes, Bruderle stated that this year they are increasing spending on social video rather than CTV.

Regarding digital, attribution is paramount.

Optimal performance is the foremost priority for the buy-side.

Black-box products such as Advantage+ from Meta and Google’s Performance Max (PMax) fail to segment campaign data based on media channel or expenditure. Nonetheless, they are securing video advertising allocations, thereby contributing to the expansion of the social video market.

Designed to optimize an advertising budget across Google or Meta inventory in order to reach the greatest number of consumers who are likely to convert. Bruderle stated that advertisers continue to invest in these products due to attribution.

Notwithstanding the compromises on transparency, advertisers communicate through their behaviors. More funds are allocated to performance metrics, while concerns regarding transparency can be postponed for a moment.

Bruderle stated that CTV requires more accurate measurement and attribution in order to contend for a greater portion of digital video advertising expenditures.

“Those publishers are making every effort to promote shoppability,” he stated. Shoppable TV strategies can assist in enhancing attribution by encouraging viewers to manipulate their remote controls, thereby increasing the signal strength of a CTV campaign. Streaming platforms are increasingly forming strategic alliances with retail media networks as they strive to achieve closed-loop attribution.

Shoppable television, however, remains largely an aspiration and not a game-changer.

Lack of transparency impedes CTV’s progress.

Advertisers place a premium on performance, but continue to appreciate transparency.

After attribution, transparency is the second factor restraining the growth of CTV advertising expenditures, according to Bruderle. The necessity for transparency in CTV advertising is particularly pressing due to the channel’s existing issue of insufficient attribution.

Understanding at the show level where advertisements aired is crucial for streaming advertisers, according to Bruderle. For years, purchasers have exerted pressure to acquire it, and they “will continue to inquire.”

In contrast to direct agreements, programmatic auctions significantly restrict transparency at the show level due to the potential violation of the Video Privacy Protection Act by publishers. A legacy from the era of Blockbuster video store records, the VPPA forbids businesses from divulging an individual’s video consumption history without their consent.

However, that does not mean publishers have no control over their content. Streamers and CTV vendors have the potential to provide a greater quantity of programming data devoid of deterministic identifiers, including aggregate reporting on impressions at the show level.

Show-level transparency is currently being incorporated into an increasing number of post-campaign reports. However, advertisers will not have access to that information for campaign planning, particularly via the bid stream, for quite some time, if ever.

Understanding the social turmoil

While advertisers desire show-level transparency, there are other forms of CTV transparency as well.

Presently, there are distinct supply routes that are incommunicative and frequently conduct multiple auctions to sell the same impression to the same customer. Therefore, advertisers cannot be certain where their ads ran or who saw them across devices, if not impossible, he explained. Thus, advertising repetition is prevalent.

The rationale for endeavors to optimize the CTV supply path in an auction with the intention of decreasing the quantity of intermediaries is this fragmentation issue. In contrast, the majority of advertisers continue to utilize direct deals, such as programmatic guaranteed deals (also known as automated insertion orders).

In regards to transparency, Bruderle stated, “CTV will reach a point.”

Bruderle predicts that in the interim, advertisers may continue to increase their spending on social media if they fail to receive the desired results from CTV sellers.